Understanding the ACT Property Market

Canberra’s Property Market Performance

If you’re thinking about buying property in Canberra, the first thing you need to understand is how the market is actually performing right now—not last year, not during COVID, but in the current cycle. And here’s the interesting part: Canberra isn’t a “boom-and-bust” market like Sydney or Melbourne. Instead, it behaves more like a steady, slow-moving machine driven by fundamentals such as government employment, stable incomes, and limited supply.

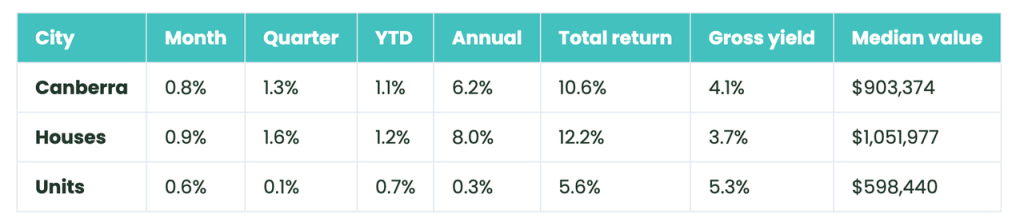

Looking at the latest data, Canberra’s property market in 2026 is showing moderate but consistent growth. Median dwelling values are sitting around $903,000+, with prices increasing roughly 1.3% over the past quarter and over 6% annually, indicating stable upward momentum rather than aggressive spikes

More information:Canberra Property Market – Prices, Trends, Forecast

A major reason for this more cautious pattern is interest rates. The Reserve Bank of Australia lifted the cash rate to 4.10% on 17 March 2026, following an earlier increase to 3.85% on 3 February 2026. Higher rates have made borrowing more expensive and reduced how much many buyers can comfortably spend, which naturally puts some pressure on demand. In other words, rate hikes have acted like a weight on the market: they have not stopped movement altogether, but they have slowed the pace and made buyers more selective. That is one reason Canberra’s market has been recovering gradually rather than accelerating too quickly.

More information:Crown leases ACT

Even with that pressure, Canberra has remained relatively resilient. One reason is that the city has strong structural support, including a large base of stable public sector employment and consistent housing demand. Another reason is supply. NAB’s February 2026 update notes that price growth is continuing to favour the house market, which reflects the fact that detached homes remain tightly held and land supply is limited in many established areas. Units, by comparison, tend to respond differently because they sit in a more price-sensitive part of the market and usually face more competition from existing and new stock.

The key takeaway is that Canberra’s market is currently stable, recovering, and highly influenced by finance conditions. Rate rises have kept affordability under pressure, but they have also prevented the kind of overheating seen in more speculative markets. At the same time, ongoing demand and limited supply have helped support prices, especially in the house segment. So if you are entering the market now, you are not stepping into chaos. You are stepping into a market where pricing is still moving upward, but where careful budgeting, strong loan preparation, and a clear property strategy matter more than ever.

Canberra’s Leasehold System

If you are researching buying property in Canberra, you need to understand one thing early. The ACT uses a leasehold system, not the standard freehold model common in other states. That sounds unusual at first. Still, in practice, most buyers can buy, sell, live in, and finance property much like elsewhere. The main difference is legal structure. In the ACT, the land remains owned by the Crown, while the buyer holds a Crown lease that sets out rights and obligations for the block. The ACT Government states that if you hold a Crown lease, you effectively own the land and property, subject to the lease terms. Residential Crown leases are usually granted for 99 years, and owners can apply for a further lease during the term.

Financial Preparation Before You Buy

Assess Your Borrowing Capacity

Before you start scrolling through listings or attending open homes, you need to know what you can realistically afford. That sounds obvious, but this step shapes everything that follows when you are buying property in Canberra. Your borrowing capacity is not just a rough number pulled from your salary. Lenders usually assess your income, living expenses, existing debts, credit limits, loan term, deposit size, and the interest rate they use for serviceability testing.

The smartest approach is to assess your borrowing capacity early, then build your property search around that number rather than around wishful thinking. It can also help you decide whether you need more deposit savings, less debt, or a lower price range before moving forward. In a market like Canberra, where affordability and competition can shift quickly, this step gives you clarity and control. You are not just asking, “What can I buy?” You are really asking, “What can I buy comfortably, safely, and with enough room to handle the unexpected?” That mindset puts you in a far stronger position before you even start.

Want a rough idea of how much you could borrow? Try the calculator below as a starting point:

Home loan borrowing power calculator

How Much Deposit Do You Need?

One of the most common questions when buying property in Canberra is simple: how much deposit do you actually need? The answer depends on both your budget and your strategy — here is what you need to know.

1.The 20% Standard

- 20% of the purchase price is widely considered the benchmark

- Helps you avoid Lenders Mortgage Insurance (LMI)

- Puts you in a stronger negotiating position with lenders

- Gives you more financial breathing room after purchase

2.Buying With Less Than 20%

- Borrowing above 80% of the property value will typically trigger LMI

- LMI protects the lender, not you, if you default on repayments

- The cost is often added directly to your loan, increasing your total repayments

- Average LMI cost: around $10,000, though this varies by loan size

3. Low Deposit Options — As Little as 5%

- Eligible first home buyers may be able to enter the market with just 5% deposit

- This is available through government-backed schemes such as the First Home Guarantee

- Eligibility rules and lender requirements still apply — not everyone will qualify

- A smaller deposit means buying sooner, but also means higher borrowing costs overall

ACT Government Grants & Concessions

1.Home Buyer Concession Scheme (HBCS)

- Administered by the ACT Revenue Office

- Reduces or fully exempts conveyance duty (stamp duty) for eligible buyers

- Full exemption available for properties up to $1,020,000 if annual household income is below $160,000

- Applies to both new and established propertie

More information:Home Buyer Concession Scheme

2.First Home Guarantee Scheme (FHBG)

- Administered by Housing Australia (Federal Government)

- Eligible first home buyers can purchase with as little as 5% deposit — no LMI required

- Government guarantees up to 15% of the property value to the lender

- Income caps: $125,000 for individuals / $200,000 for couples

- Property price cap in ACT: check current limits on the official site

More information:First Home Buyer ACT

3.First Home Super Saver Scheme (FHSSS)

- Administered by the Australian Taxation Office (ATO)

- Withdraw voluntary super contributions (made since 1 July 2017) toward your deposit

- Up to $50,000 per individual / $100,000 per couple

- Tax benefit: super contributions taxed at 15%, lower than most personal income tax rates

More information:First Home Super Saver Scheme

Step-by-Step Process of Buying Property in Canberra

← swipe or use buttons →

Costs Involved in Buying ACT Property

Upfront Costs You Need to Budget For

When you are buying property in Canberra, the deposit is only the beginning. The real upfront budget usually includes a cluster of costs that arrive together, and they can shape your buying power just as much as the purchase price itself. That is why smart buyers do not treat these as side notes. They treat them as part of the entry ticket. For anyone researching buying ACT property, especially a first home buyer in the Canberra audience, understanding these costs early makes the whole process feel less like walking through fog and more like following a map. In practical terms, your upfront budget should usually cover your deposit, conveyance duty, legal and conveyancing fees, inspection costs, lender fees, and any Lenders Mortgage Insurance (LMI) that may apply if your deposit is below 20%. In the ACT, private treaty purchases generally have a five-day cooling-off period, while auctions do not, which makes financial readiness even more important before you commit.

- Deposit

Your deposit is the main upfront cost and affects how much you need to borrow. A larger deposit can reduce pressure on your loan and may help you avoid extra costs.

- Conveyance Duty

This is the ACT tax charged on property transfers. The amount depends on the property value and whether you qualify for any concessions.

- Legal & Conveyancing Fees

These are the professional fees for reviewing the contract, handling the legal process, and completing settlement.

- Building & Pest Inspection Fees

These costs cover inspections that help identify structural issues or pest problems before you commit to the purchase.

- Loan & Lender Fees

These may include loan setup or administration fees charged by your lender when arranging the mortgage.

- Lenders Mortgage Insurance (LMI)

LMI usually applies when your deposit is below 20%. It protects the lender and adds to the overall cost of buying.

Ongoing Costs After Settlement

Getting the keys does not mean the spending stops. Once settlement is complete, the focus shifts from purchase costs to the ongoing expenses of ownership, and these are the costs that quietly shape your monthly and yearly budget over time. When people think about buying property in Canberra, they often prepare carefully for the deposit and legal process, then underestimate what it takes to hold the property comfortably after move-in day. That is why this part of the guide matters. Ongoing costs are not as dramatic as the upfront ones, but they are the bills that keep showing up long after the excitement fades. For anyone planning to buy a home in the ACT, especially a first-home buyer in the Canberra audience, these expenses should be treated as part of affordability, not as an afterthought. In the ACT, this can include council rates, land tax where applicable, strata fees for units or townhouses, home and contents insurance, and the everyday running costs of utilities and maintenance. Recent ACT budget settings also point to continuing ownership costs, with average general rates in 2025–26 increasing by 3.75% for residential and commercial properties.

- Council Rates

A regular property ownership cost charged in the ACT and should be included in your ongoing budget.

- Land Tax

Usually applies to investment properties rather than owner-occupied homes, but it is still important to understand early.

- Strata Fees

Ongoing fees for apartments or townhouses that help cover shared property maintenance and management costs.

- Home & Contents Insurance

Insurance helps protect the building, your belongings, or both, and should be treated as an essential ownership cost.

- Utilities & Maintenance

Regular living costs such as electricity, water, and internet, plus ongoing repairs and property upkeep.

Why Full-Cost Budgeting Matter

A full-cost budget matters because the price on the listing is rarely the price you actually need to be ready for. When buying property in Canberra, buyers are not just paying for the home itself. They are also stepping into a chain of extra costs that can quickly change what feels affordable, from the deposit and conveyance duty to legal fees, inspections, lender charges, and the ongoing expenses that continue after settlement. In the ACT, timing also matters because private treaty purchases usually come with a five-day cooling-off period, while auctions and tenders generally do not, which means your finances often need to be organised before the pressure hits.

This is why full-cost budgeting is less about being cautious and more about being realistic. It helps you set a true price range, protect your savings buffer, and avoid stretching yourself just to secure the property. That is especially important for a first-home buyer Canberra audience, where the excitement of getting into the market can sometimes make the hidden costs feel smaller than they really are. A clear budget lets you ask the better question: not just “Can I afford this property?” but “Can I afford everything that comes with it?” That shift usually leads to stronger decisions, less stress, and a much smoother path through the buying process.

Expert Tips for Buying Property in Canberra

General Advice

Research suburbs carefully, understand the ACT buying process, and get your finance sorted early. Leave room in your budget for more than just the purchase price, including duty, legal costs, and inspections. In Canberra, it is also important to review the contract documents carefully, not just the property itself.

First Home Buyers

Focus on affordability, transport, lifestyle, and long-term growth before choosing a property. Check whether you may be eligible for any home buyer assistance or concession schemes, because this can affect your real budget. Get pre-approval early and know exactly what price range feels manageable before you start making offers.

Investors

Look beyond appearance and focus on rental demand, land tax, ongoing costs, and long-term value. Choose suburbs and property types that align with your investment strategy rather than short-term trends. A strong investment decision should balance purchase price, holding costs, and future growth potential.